According to Amnesty International in its report ‘Broken and unequal: The state of education in South Africa’, published in 2020, South Africa has one of the most unequal school systems in the world. The report quotes Nic Spaull, Senior Researcher at the University of Stellenbosch…

“…South Africa today is the most unequal country in the world. The richest 10% of South Africans lay claim to 65% of national income and 90% of national wealth; the largest 90-10 gap in the world. These inequities are mirrored in the education system where we have 20% of schools that are broadly functional, and 80% that are mostly dysfunctional. Because of this, two decades after apartheid it is still the case that the life chances of the average South African child are determined not by their ability or the result of hard-work and determination, but instead by the color of their skin, the province of birth, and the wealth of their parents. These realities are so deterministic that before a child’s seventh birthday one can predict with some precision whether they will inherit a life of chronic poverty and sustained unemployment or a dignified life and meaningful work. The sheer magnitude of these inequities is incredible…”

The above photo of a school near Peddie in the Eastern Cape is courtesy of the Amnesty International report

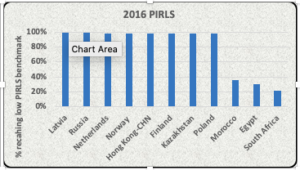

The Amnesty International report continues to haunt with frightening statistics about our 23,471 public schools. 19% of these schools have pit latrines, 86% have no laboratories and 72% have no internet access. Good luck President Ramaphosa with your initiative to provide every school child with digital workbooks and textbooks on a tablet device. Good luck to the Department of Basic Education (DBE) with their plan to introduce coding into the school syllabus. According to the Progress in International Reading Literacy Study (PIRLS) 2016 report published by the U.S. Department of Education, only 22% of South African grade 4 pupils can read for meaning (implying that 78% of grade 4 learners have no comprehension of what they are seeing on a page). How is it possible to have such a large gap in reading ability between the likes of Latvia and Poland as compared with South Africa? How on earth will public school kids be able to read on their tablets without internet access? The mind boggles at our government who seem completely removed from reality.

According to Spaull, for every 100 learners starting school in South Africa, 60 will write matric and 37 will pass (not that hard to do given the DBE’s standards). Of those who embarked upon the journey 12 or 13 years previously, 14% will achieve a Bachelor pass and 12% will go to university. Only 4% of the learner cohort which started school will attain an undergraduate degree within 6 years of starting their university journey. We have a public education system that is broken beyond repair. It is taking some willpower not to reach for some amber nectar.

The above mentioned crisis has provided an opportunity for certain entrepreneurs to benefit from the government’s ineptitude. The likes of Curro and ADvTECH have built private educational businesses focusing on both school and tertiary education. I have followed Curro with great interest over the years, particularly their share price which beggars belief. I have often used them as a case study in valuation workshops and seminars. I have never been able to arrive at a fair value per share in the same hemisphere as the stock market. The market seems to have come to its senses as Curro’s share price has dropped from a peak of R60 in late 2015 to current levels of around R12.

Curro recently released its results for the year ended 31 December 2019 (FY2019). I have updated my Excel model analyzing their results – refer attached.Curro Analysis (Feb 2020) Learner numbers were over 57,000 in FY2019 and revenue has almost reached R3 billion. For a business that started in 1998, the growth has been phenomenal. However, I have some concerns about their numbers:

- Curro pays very limited income tax. In FY2019, their effective tax rate was 6.9% versus the statutory rate of 28%. At some point in time, Curro’s taxation payments should edge up to the 28% level. I am always suspicious of corporates that pay very low income tax;

- Curro’s debt levels are dangerously high for my liking. I get that private schools are relatively low risk businesses once they have matured. Parents, who encounter financial difficulty, are loath to move their children out of expensive schools to more affordable options. Rational parents are more likely to cut expenditure such as DSTV, life and short-term insurance than change schools. Curro’s interest-bearing debt at the end of FY2019 was R3.9 billion, which was 5 times adjusted EBITDA (earnings before interest, taxation, depreciation and amortization). Credit rating agencies generally rank corporate debt as junk status once debt to EBITDA reaches 5.5 times; and

- Curro’s fixation with publishing its J-Curve which sets out the EBITDA margins (EBITDA divided by revenue) of schools by year in which they started. Curro seems to want to convince the stock market that school’s EBITDA margins improve with age. I get that but tend to have a WeWork moment reading it. It goes like this…The total market for private school learners is x, we aim to capture x% of the market hence, there is enormous scope for growth…buy our shares, its a great investment.

Anyway, it’s just my opinion. I think Curro has a good business model and plays an important role in plugging the gap left by government and top fee private schools. They say that stock markets like revenue and profit growth and rewards these companies with atmospheric share prices. However, be careful of the day that you disappoint the stock market with lower than expected profits…the retribution is swift and nasty. Anyway, take care out there and all the best from BeechieB.

Recent Comments