When the Johannesburg Stock Exchange (JSE) introduced the requirement for listed companies to disclose the remuneration of executive directors in the early 2000s, I was on record warning about the unintended consequences of this. I argued that by making executive pay public knowledge, the average remuneration of directors would generally rise as individuals demanded comparative pay to their peers. Previously, executive remuneration was not in the public domain and hence, it was difficult for executives to benchmark executive pay except anecdotally.

The Companies Amendment Bill of 2021 in South Africa proposes taking disclosure of executive remuneration a step further. It proposes the disclosure by state-owned and public companies of:

- the total remuneration (guaranteed salary, benefits and other incentives) that has been paid to the highest paid employee and that of the lowest paid employee

- the average and median remuneration of all employees

- the gap, expressed as a ratio, between the top 5% highest paid employees and the bottom 5% lowest paid workers

The U.S. Securities and Exchange Commission (SEC) introduced similar disclosure requirements in 2015 for all listed USA companies. Their requirements are simpler requiring only the disclosure of what the CEO earns versus the median (mid-point in the data set) of all its employees except the CEO. The Marxist leanings of the ANC government is clearly evident in the Companies Amendment Bill 2021, requiring public and state-owned companies to publish what the highest and lowest paid employees earn, which will reveal a much worse pay gap than comparing the CEO’s paycheck to the median salary of all employees. I also venture to guess that the pay gap ratio at our bloated state-owned entities will be much lower than in the private sector.

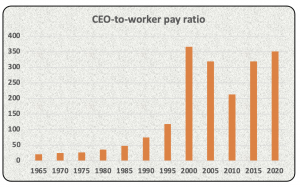

The Economic Policy Institute based in Washington D.C, recently published the CEO-to-worker compensation ratio (average remuneration of CEO versus the average worker in that firm’s industry). According to their calculations, CEOs earned 351 times more than the average pay packet of all employees. This ratio reached a peak in 2000 during the dot.com boom but 2020’s result, whilst in the midst of a pandemic, is near that peak.

As can be seen in the above chart, the CEO-to-worker pay ratio was ±20 times in 1965. It has increased steadily over time, which may be due to lucrative share incentive schemes which enrich the top executives rather than the masses.

McDonald’s CEO, Chris Kempczinski, earned a total of US$10.8 million in 2020 which was 1,189 times higher than the median salary (US$9,122) of McDonald’s employees. The pay ratio is calculated as CEO remuneration divided by the global median salary of McDonald’s workers. I would be guessing that a griller in Phuket, Thailand would not be earning the same as his/her counterpart in New York.

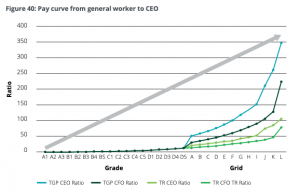

Deloitte in its September 2021 report, “Your guide: Director and prescribed officer remuneration at JSE listed companies”, reveals that the total guaranteed pay (TGP) of CEOs versus the general worker of JSE listed companies is similar to the USA experience. Magically, the ratio of 350 times in RSA is near damn it to the USA’s 351 times.

PS. Andre de Ruyter, the CEO of Eskom, earned R7.2 million in the year ended 31 March 2021, which was 9.5 times that of the average of all Eskom employees (±R748,626).

The Economic Policy Institute estimated that the average realized remuneration of CEOs of USA listed companies was US$24.2 million in 2020. That would imply that the average worker pay was ±US$69,000 in 2020. This is similar to the US Census Bureau’s published data of median household income of US68,703 in 2019. I have some sympathy for those who argue that executive compensation is generally too high relative to their actual inputs and versus the general worker. Imagine earning US$24.2 million a year (±R363 million) for barking orders and traveling business class and occasionally having to explain things at a board meeting?

PWC’s “Practices and remuneration trends report, August 2021”, reveals that the average pay packet of CEOs of JSE listed companies was R5.2 million in 2020 whilst the average CEO pay in the larger listed consumer goods companies was a whopping R38.7 million. It would appear that South African executives are significantly underpaid relative to their USA peers (dry humor intended, no offense meant).

I wonder what the intentions are behind forcing the disclosure of the highest paid employee versus the lowest paid, and the pay gap between the top 5% and bottom 5%? Well, the Companies Amendment Act Bill published on 1 October 2021, had some interesting statements in this regard:

“…Excessive remuneration particularly at the highest levels of a company is a matter of great concern internationally…”

“…The factors giving rise to these concerns are to an extent responsible for the significant levels of inequity in society…”

“…The amendments proposed in the Bill are also required to tackle the injustice of excessive pay. The pay gap has been a historical challenge and a contributor to the country’s inequality…”

“…Analysis of Statistics South Africa data in the annual Labour Market Dynamics survey shows that inequality in pay contributes as much to overall income inequality as joblessness…”

“…This kind of inequality underpins much of the well-known workplace conflict in South Africa…”

Ok, I get it. The reason for inequality and inequity in society is that executives are paid so much more than lowly workers. Our Minister of Trade, Industry and Competition, the notorious communist Ebrahim Patel, seems to think that the answer to South Africa’s dire unemployment and inequality problems are to simply force those capitalist pigs to disclose what they earn. Perhaps a better way of reducing income inequality would be to pay all workers the same irrespective of education, skill, know-how and experience levels? That would certainly solve the inequality problem. Furthermore, perhaps nationalizing everything would solve wealth inequality too since all of us except those communists at the top would have no assets. I am being facetious. There are some very clever economists and business people out there who could provide some solid suggestions to reducing unemployment and inequality. I don’t trust these ANC cadres and their advisors to solve anything. Rather I expect them to blame everyone else for destroying the South African economy and creating world leading unemployment levels.

If these disclosure rules are enforced, what do I think may transpire?

- Public companies will continue to pay their executives millions, ignoring the bleating regulators;

- Companies will find ingenious ways to hide elements of executive compensation;

- Companies may embark on African and international expansion, limiting investment in South African operations;

- The trade unions will demand higher wages for their members by highlighting the enormous pay gaps;

- Companies may aggressively replace lower skilled and paid employees with robots and automation;

- Companies may outsource more of their operations; and/or

- Rising unemployment levels in South Africa.

Beware the unintended consequences of decisions

Have fun out there and celebrate the municipal election results. Service delivery is set to improve in certain areas. All the best from BeechieB.

I remember the video footage of hospitals in Northen Italy in March 2020 – it was a horror show. Unfortunately, Italy paid a heavy COVID-19 price, with one the worst per capita deaths globally. Have you noticed how the waves in adjacent countries occur in very similar time periods, albeit that the severity may differ?

I remember the video footage of hospitals in Northen Italy in March 2020 – it was a horror show. Unfortunately, Italy paid a heavy COVID-19 price, with one the worst per capita deaths globally. Have you noticed how the waves in adjacent countries occur in very similar time periods, albeit that the severity may differ?

Here again, COVID-19 deaths occurred irrespective of the draconian quarantine measures in the UK. Mortality rates from or with COVID-19 in Belgium and the UK were both in the top 5 in the world as at February 2021.

Here again, COVID-19 deaths occurred irrespective of the draconian quarantine measures in the UK. Mortality rates from or with COVID-19 in Belgium and the UK were both in the top 5 in the world as at February 2021. I warned you that charts can sometimes deflect from the real story. Well, Bulgaria got blitzed by COVID-19 and by 8 March 2021, the country had recorded 162 deaths per 100,000 population. Turkey fared far better at 35 deaths per 100,000. Bulgaria has a population of ±7 million whereas Turkey is far more populous at 84 million.

I warned you that charts can sometimes deflect from the real story. Well, Bulgaria got blitzed by COVID-19 and by 8 March 2021, the country had recorded 162 deaths per 100,000 population. Turkey fared far better at 35 deaths per 100,000. Bulgaria has a population of ±7 million whereas Turkey is far more populous at 84 million.

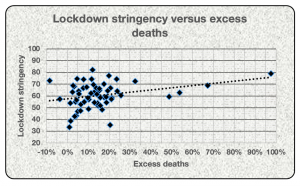

If the data from the USA and Canada does not convince you to question whether lockdown measures have any impact on halting the SARS-CoV-2 virus spreading through the population, then you may be visually impaired. I know the USA is a vast country comprising 50 different states and hence, it may not be accurate to compare the country as whole to other countries. From the published data I have seen, COVID-19 mortality rates have varied from state to state and without much correlation to lockdown measures.

If the data from the USA and Canada does not convince you to question whether lockdown measures have any impact on halting the SARS-CoV-2 virus spreading through the population, then you may be visually impaired. I know the USA is a vast country comprising 50 different states and hence, it may not be accurate to compare the country as whole to other countries. From the published data I have seen, COVID-19 mortality rates have varied from state to state and without much correlation to lockdown measures. Oh my goodness, I was questioning whether I had extracted the appropriate data, so I double checked. Yip, the data accords with the original sources. So how do you explain that 11 of the countries with the worst performing economies in 2020 also had some of the highest COVID-19 mortality? It makes no sense at all. It gets worse.

Oh my goodness, I was questioning whether I had extracted the appropriate data, so I double checked. Yip, the data accords with the original sources. So how do you explain that 11 of the countries with the worst performing economies in 2020 also had some of the highest COVID-19 mortality? It makes no sense at all. It gets worse. My hypothesis is now completely threaded. 12 countries whose economies escaped relatively unscathed in 2020 also had very low COVID-19 mortality rates. I am calling on all economists, public health officials, epidemiologists, virologists, actuaries and any credible scientist to explain the above data. Using Excel’s CORREL function, the correlation between COVID-10 outcomes and GDP data for the 55 selected countries, was -91%. Countries with high COVID mortality most of the time had poor economic outcomes in 2020 whilst countries that had low COVID-19 mortality achieved better economically. It is inexplicable to me.

My hypothesis is now completely threaded. 12 countries whose economies escaped relatively unscathed in 2020 also had very low COVID-19 mortality rates. I am calling on all economists, public health officials, epidemiologists, virologists, actuaries and any credible scientist to explain the above data. Using Excel’s CORREL function, the correlation between COVID-10 outcomes and GDP data for the 55 selected countries, was -91%. Countries with high COVID mortality most of the time had poor economic outcomes in 2020 whilst countries that had low COVID-19 mortality achieved better economically. It is inexplicable to me.

To be fair, the DBE had not yet released the Western Cape’s matric results by the time of publishing the NSC report, so an Excel or Numbers file may in the offing. Talking about NSC results, I was deeply disturbed by the raw data. Perhaps I should not have read the report and examined how poorly our 18 year olds (some may be younger and some may be older) performed in their final written assessments. Approximately 40% of the total cohort took mathematics in grade 12 and wrote the exam. Of those, 22% managed to obtain a mark of 50% or more. Sadly, only 3.2% achieved a distinction. I am not sure how employable you would be in the future smart city around Lanseria and amidst the Fourth Industrial Revolution without a reasonable mathematics foundation.

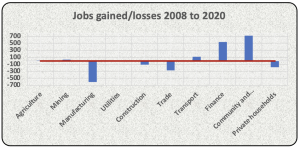

To be fair, the DBE had not yet released the Western Cape’s matric results by the time of publishing the NSC report, so an Excel or Numbers file may in the offing. Talking about NSC results, I was deeply disturbed by the raw data. Perhaps I should not have read the report and examined how poorly our 18 year olds (some may be younger and some may be older) performed in their final written assessments. Approximately 40% of the total cohort took mathematics in grade 12 and wrote the exam. Of those, 22% managed to obtain a mark of 50% or more. Sadly, only 3.2% achieved a distinction. I am not sure how employable you would be in the future smart city around Lanseria and amidst the Fourth Industrial Revolution without a reasonable mathematics foundation. The manufacturing sector has been a blood bath with a loss of 607,000 jobs over the past 12 years. Employment conditions in the construction and trade (I assume retail) sectors have not been great either. Interestingly, the finance sector has created 543,000 jobs whilst the ‘community and social services’ sector added 720,000 odd jobs. I am guessing that the community and social services jobs entail mostly public sector employment, those fine people in parliament and in education and in healthcare. The latter hare to be applauded for their efforts amidst this pandemic. The educators less so.

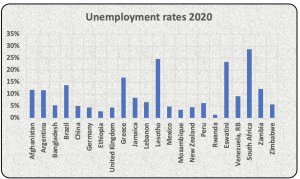

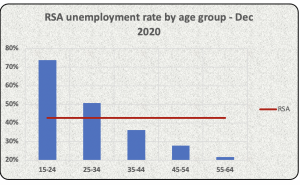

The manufacturing sector has been a blood bath with a loss of 607,000 jobs over the past 12 years. Employment conditions in the construction and trade (I assume retail) sectors have not been great either. Interestingly, the finance sector has created 543,000 jobs whilst the ‘community and social services’ sector added 720,000 odd jobs. I am guessing that the community and social services jobs entail mostly public sector employment, those fine people in parliament and in education and in healthcare. The latter hare to be applauded for their efforts amidst this pandemic. The educators less so. The expanded unemployment rate amongst 15 to 24 year old South Africans was a staggering 74% in the last quarter of 2020. Amongst 25 to 34 year olds, it was 51%. It seems the older are less afflicted. The median age in South Africa is 27 and 54% of our population is under the age of 30. I would opine that we have a humanitarian crisis in South Africa with regards to employment and unemployment levels.

The expanded unemployment rate amongst 15 to 24 year old South Africans was a staggering 74% in the last quarter of 2020. Amongst 25 to 34 year olds, it was 51%. It seems the older are less afflicted. The median age in South Africa is 27 and 54% of our population is under the age of 30. I would opine that we have a humanitarian crisis in South Africa with regards to employment and unemployment levels. Picture courtesy of the New York Times

Picture courtesy of the New York Times

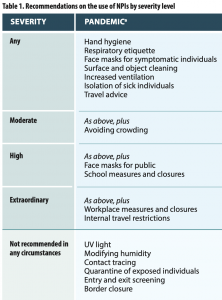

Notice that increased ventilation is recommended and not beach closures. Notice that contact tracing and quarantine of exposed individuals (aka lockdowns) are not recommended in any circumstances. And no border closures please! The WHO’s views on school closures in their 2019 document seems balanced and sensible, I quote:

Notice that increased ventilation is recommended and not beach closures. Notice that contact tracing and quarantine of exposed individuals (aka lockdowns) are not recommended in any circumstances. And no border closures please! The WHO’s views on school closures in their 2019 document seems balanced and sensible, I quote:

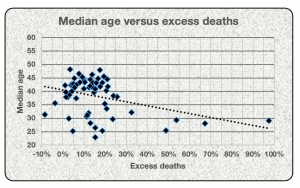

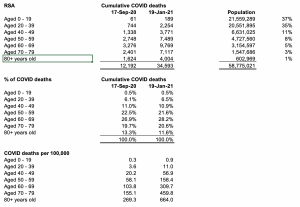

South Africa has a youthful population – ±72% of our population is under the age of 39 with a median age of 27. SARS-Cov-2 is particularly severe for the elderly and South Africa’s data supports this. Notice the much higher deaths per 100,000 for 70+ year olds as compared to the 20 to 39 age bracket? Our age based COVID mortality is not great compared to most European countries but that is another blog post on its own. COVID deaths have dramatically increased in the past 4 months. The percentage of total COVID deaths per age profile is very similar to what it was 4 months ago, not supporting the theory of the second wave hitting younger people harder than previously. Over 60% of all deaths from COVID to date in South Africa were people 60 yers or older.

South Africa has a youthful population – ±72% of our population is under the age of 39 with a median age of 27. SARS-Cov-2 is particularly severe for the elderly and South Africa’s data supports this. Notice the much higher deaths per 100,000 for 70+ year olds as compared to the 20 to 39 age bracket? Our age based COVID mortality is not great compared to most European countries but that is another blog post on its own. COVID deaths have dramatically increased in the past 4 months. The percentage of total COVID deaths per age profile is very similar to what it was 4 months ago, not supporting the theory of the second wave hitting younger people harder than previously. Over 60% of all deaths from COVID to date in South Africa were people 60 yers or older.

I had some spare time this week so I downloaded the Airbnb prospectus and had a long read – the document was over 489 pages! Here are some interesting facts about Airbnb:

I had some spare time this week so I downloaded the Airbnb prospectus and had a long read – the document was over 489 pages! Here are some interesting facts about Airbnb:

You may recall Dr Ngubane’s (chairperson from 2010 to 2013) antics at the SABC and subsequently as Eskom chairperson. Ms Suzanne Vos made some damning statements about Dr Nbubane to the Parliamentary Monitoring Group in March 2013 following the mass resignations from the SABC board. She stated that Dr Ngubane was prone to making unilateral decisions without consulting the rest of the board of directors. He attempted to overturn board decisions such as the relieving Hlaudi of his position as acting COO. Dr Ngubane apparently also failed to attend meetings if he was angry or did not get his own way. That type of behavior clearly works as he was then entrusted to chair Eskom through difficult times. He was spectacularly unsuccessful at that and we are all living with the consequences of irregular power and another debt laden SOE (refer an earlier blog about Eskom and its inability to trade out of its debt burden).

You may recall Dr Ngubane’s (chairperson from 2010 to 2013) antics at the SABC and subsequently as Eskom chairperson. Ms Suzanne Vos made some damning statements about Dr Nbubane to the Parliamentary Monitoring Group in March 2013 following the mass resignations from the SABC board. She stated that Dr Ngubane was prone to making unilateral decisions without consulting the rest of the board of directors. He attempted to overturn board decisions such as the relieving Hlaudi of his position as acting COO. Dr Ngubane apparently also failed to attend meetings if he was angry or did not get his own way. That type of behavior clearly works as he was then entrusted to chair Eskom through difficult times. He was spectacularly unsuccessful at that and we are all living with the consequences of irregular power and another debt laden SOE (refer an earlier blog about Eskom and its inability to trade out of its debt burden). The ANC seemed to take the Department of Communications seriously at the start of its rule by appointing heavyweights such as Pallo Jordan to oversee matters. Unfortunately, some of the appointees over the past 10 years had questionable reputations. Dina Pule was apparently adept at lying and cheating to benefit her then boyfriend back in the days. Faith Muthambi has been implicated in state capture given evidence at the Zondo Commission. She must have done some naughty stuff for OUTA to have laid treason and corruption charges against her in 2017. Mention Nomvula Mokonyane and I think Bosasa and Xmas braai packs. Stella Ndabeni-Abrahams was caught flagrantly disregarding lockdowns regulations earlier in 2020. She is now in the news for overturning the SABC board of directors decision to retrench 400 employees. Perhaps Stella needs to do a Corporate Governance 101 refresher.

The ANC seemed to take the Department of Communications seriously at the start of its rule by appointing heavyweights such as Pallo Jordan to oversee matters. Unfortunately, some of the appointees over the past 10 years had questionable reputations. Dina Pule was apparently adept at lying and cheating to benefit her then boyfriend back in the days. Faith Muthambi has been implicated in state capture given evidence at the Zondo Commission. She must have done some naughty stuff for OUTA to have laid treason and corruption charges against her in 2017. Mention Nomvula Mokonyane and I think Bosasa and Xmas braai packs. Stella Ndabeni-Abrahams was caught flagrantly disregarding lockdowns regulations earlier in 2020. She is now in the news for overturning the SABC board of directors decision to retrench 400 employees. Perhaps Stella needs to do a Corporate Governance 101 refresher.

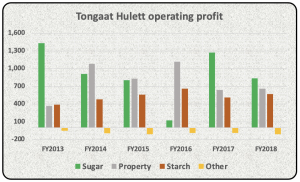

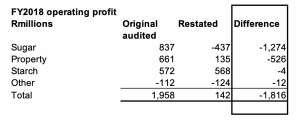

The Sugar division’s operating profit of R837 million descended into a loss of R437 million in FY2020 due to the aforementioned reasons. The Property division was also apparently a bit naughty, recording land sales upon signature of agreements rather than upon transfer. The division also saw fit to occasionally lend money to potential buyers to fund the acquisition of properties from Tongaat. No wonder Hudson and his team were struggling to collect some of their debtors book during 2019.

The Sugar division’s operating profit of R837 million descended into a loss of R437 million in FY2020 due to the aforementioned reasons. The Property division was also apparently a bit naughty, recording land sales upon signature of agreements rather than upon transfer. The division also saw fit to occasionally lend money to potential buyers to fund the acquisition of properties from Tongaat. No wonder Hudson and his team were struggling to collect some of their debtors book during 2019.

Recent Comments