The proposed sale of a 20% shareholding in a new entity to be created to hold the commercial rights and interests of the South African Rugby Union (SARU) to an obscure USA private equity outfit called Ackerley Sports Group (ASG) has elicited major criticism by some. The meeting to vote on the deal was scheduled for 17 October 2024 but has been postponed to December 2024 amidst backlash from inter alia, the Bulls, Sharks , Golden Lions and the Stormers franchises, the Minister of Sport, Arts & Culture, the Honorable Mr. Gayton McKenzie, and SARU’s major broadcast partner, Supersport. Imagine constructing a deal that pisses off your major partners being the RSA unions participating in the United Rugby Championship and Supersport? This could be a fascinating ‘business school’ case study how not to do a deal.

For those who have not read and/or reviewed the proposed SARU/ASG deal, as leaked by Business Day on 14 October 2024, the key elements of this imaginative corporate action include :

- A new company, SARU Commercial Rights Company (CRC), will be formed to own all the commercial rights of SARU including the invaluable Springbok brand

- SARU and ASG will own 80% and 20% equity interests in CRC respectively

- Upon closing of the deal, ASG will advance a $35 million loan to CRC

- ASG undertakes to advance a further loan tranche of $15 million 18 months after deal closing

- ASG undertakes to advance final two tranches of $15 million and $10 million in 18 month intervals after the first $15 million advance but subject to undisclosed performance metrics

- The board of directors of CRC will consist of 7 directors of which ASG and SARU will each be entitled to appoint 3 directors. An independent chairperson will be appointed by ASG [sic]

- 90% of the net cash flows generated by CRC will be first applied to repaying ASG’s loan account together with 8% compound interest

- Once ASG’s loan (and interest) has been fully repaid, SARU and ASG will each presumably share in 80% and 20% respectively of the dividends declared by CRC

An interesting aspect of the above deal structure is the scheduled loan repayments to and loan advances by ASG. The leaked PowerPoint presentation included forecast cash flows to and from ASG.

So ASG could be funding some of its loan advances using the proceeds of loan repayments from CRC – excellent negotiating and structuring by ASG. Private equity players, take note of this innovative investment structure, it could make you billions using other peoples’ money.

Tiisetso Motsoeneng, writing in the Business Day on 22 October 2024, launched into a scathing attack on the proposed SARU/ASG deal. Inter alia, Motsoeneng alleges that “…the valuation of the Springbok’s commercial rights at $375 million is a glaring underestimation…”. He further criticizes the deal for giving up control over the Springbok brand and legacy.

The Sharks, Bulls, Golden Lions, Stormers, Cheetahs, Boland Rugby Union and the Griquas prepared and signed a 7 page letter detailing their objections to the proposed ASG deal. There were compelling arguments against the deal and they questioned the potential value add of ASG. The proposed transaction fee payable of $7.5 million to Eddie Jordan, erstwhile F1 racing driver, also elicited a strong rebuke. What value could a transaction adviser add to justify a 10% transaction fee? PS note to self, next time I bid for a corporate finance mandate, refer to Jordan’s 10% fee structure in justification for my paltry 5% success fee.

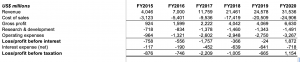

I decided to trawl through SARU’s annual reports for the years ended December 2019 through to December 2023. I expected to find some trauma relating to the COVID-19 pandemic lockdowns. Turns out, SARU encounters drama most years, battling to breakeven and not incur operating losses. Mark Alexander, the SARU chairperson, in the FY2023 annual report refers to the malaise facing SARU stating “…at the onset of 2023, our organization was confronted with a budget shortfall of R254 million, a direct consequence of the enduring impacts of the pandemic, our departure from Super Rugby, and our strategic investments in the north to preserve the professional game at home…”.

My analysis of SARU’s financial performance and position over the period FY2019 to FY2023 is included in the attached Excel spreadsheet. SA Rugby Analysis (October 2024). SARU managed to pull off miracles in FY2021 when the British & Irish Lions tour (without spectators) managed to generate R396 million in revenue for SARU. In FY2023, SARU managed to increase its grant income from World Rugby from R36 million in FY2022 to R291 million in FY2023. Without these two windfalls, SARU may have had serious going concern issues.

Frankly, having reviewed SARU’s historical financial performance, I would not invest my own money in SARU. The organization has reported operating losses in the past two years and pressures seem ongoing. Any business is only worth what it can produce in profits and free cash flows in the future. In SARU’s case, I applaud the executive for finding a private equity fund who is prepared to value the commercial rights of SARU at circa $375 million. Perhaps that’s why the deal structure was so overwhelming structured in favor of ASG?

Perhaps the debate should be whether SARU should be a capitalistic entity seeking to maximize profits for its shareholders or it should be a non-for-profit organization? The proposed CRC aiming to generate increasing profits and cash flows for ASG and SARU seems fraught with agency costs and conflicts of interests?

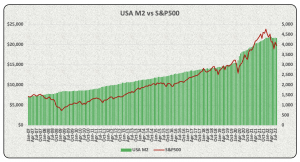

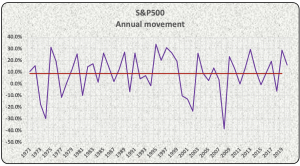

The correlation between M2 money supply data and the movements in the S&P500 index over the ±52 year period was 97%. I know, I know, I know. You are taught at university that correlation does not equate to causation. But a 97% correlation is no coincidence.

The correlation between M2 money supply data and the movements in the S&P500 index over the ±52 year period was 97%. I know, I know, I know. You are taught at university that correlation does not equate to causation. But a 97% correlation is no coincidence.

The dude’s name is Sam Bankman-Fried (pronounced “Freed” and not like Kentucky “fried” chicken), a 30 year old who founded and controlled a cryptocurrency exchange called FTX. He was also CEO of Alameda Research, a quantitative cryptocurrency trading firm. FTX filed for bankruptcy on 11/11/22 (a rather symmetrical date). Forbes has estimated Bankman-Fried (SBF) was once worth US$32 billion but earlier today reported that he only had US$100,000 left in the bank. Hard to believe that, I am sure that he has many millions hidden away in offshore tax friendly jurisdictions. SBF’s parents are both law professors at Stanford University. His father is also a clinical psychologist who specializes in treating young adults suffering from anxiety and depression. I am sure Professor Bankman-Fried will have some comforting words for his son. SBF’s mother is reportedly a tax expert, and focuses on moral philosophy and distributive justice. I had to google the last term, never heard of it before today. Mrs Google tells me that “distributive justice” is about socially just allocation of resources. I am surprised the ANC has not cottoned onto “distributive justice” but give them time. Their last election slogan “building better communities together” did not translate into reality with load shedding, crumbling water infrastructure and sewerage flowing into rivers and oceans. I digress.

The dude’s name is Sam Bankman-Fried (pronounced “Freed” and not like Kentucky “fried” chicken), a 30 year old who founded and controlled a cryptocurrency exchange called FTX. He was also CEO of Alameda Research, a quantitative cryptocurrency trading firm. FTX filed for bankruptcy on 11/11/22 (a rather symmetrical date). Forbes has estimated Bankman-Fried (SBF) was once worth US$32 billion but earlier today reported that he only had US$100,000 left in the bank. Hard to believe that, I am sure that he has many millions hidden away in offshore tax friendly jurisdictions. SBF’s parents are both law professors at Stanford University. His father is also a clinical psychologist who specializes in treating young adults suffering from anxiety and depression. I am sure Professor Bankman-Fried will have some comforting words for his son. SBF’s mother is reportedly a tax expert, and focuses on moral philosophy and distributive justice. I had to google the last term, never heard of it before today. Mrs Google tells me that “distributive justice” is about socially just allocation of resources. I am surprised the ANC has not cottoned onto “distributive justice” but give them time. Their last election slogan “building better communities together” did not translate into reality with load shedding, crumbling water infrastructure and sewerage flowing into rivers and oceans. I digress.

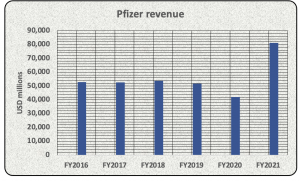

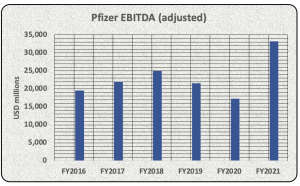

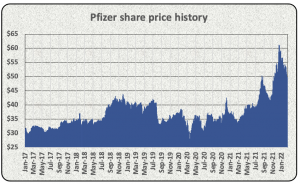

The above chart depicts Pfizer’s stagnating revenue until FY2021. Revenue in FY2020 was USD41.9 billion, in 2021 it increased by 94%. Not too shabby at all. And there is more good news to come since management are forecasting to produce 4 billion COVID-19 vaccines in 2022. They also have a new oral COVID medication called Paxlovid coming onto the market, having received FDA emergency use approval in December 2021. December seems to be a very good month for them. Management are optimistic that Paxlovid will deliver USD22 billion of revenue for the group in FY2022.

The above chart depicts Pfizer’s stagnating revenue until FY2021. Revenue in FY2020 was USD41.9 billion, in 2021 it increased by 94%. Not too shabby at all. And there is more good news to come since management are forecasting to produce 4 billion COVID-19 vaccines in 2022. They also have a new oral COVID medication called Paxlovid coming onto the market, having received FDA emergency use approval in December 2021. December seems to be a very good month for them. Management are optimistic that Paxlovid will deliver USD22 billion of revenue for the group in FY2022.

Recent Comments